Login to access Everything Marketplaces

Don't have a member account? Join here.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

We're sharing a blog post from Mike Williams with a comprehensive guide on fundraising for marketplaces with benchmarks and valuations for 2026. This was previously shared as a post in the community here.

Hey all, I’m sharing a long overdue 10+ page guide I put together on fundraising for marketplaces with benchmarks & valuations for 2026. I ran this by other marketplace investors like FJ Labs, NFX, Headline, Forerunner, Snak VC, Yonder Ventures, used data from what we’re seeing at Marketplace Capital, and also referenced Carta and AngelList data to help inform the guide. You can see the accompanying resources at the end and I'd love to hear what you're seeing in the market in the comments below.

The rules of marketplace fundraising have changed. During the 2020-2021 venture boom, rapid GMV growth was often enough to justify large raises, even when core fundamentals were weak. That playbook is gone.

Today's investors evaluate efficiency alongside velocity. Retention quality, take rate durability, CAC payback periods, contribution margins, and capital efficiency matter as much as growth rate. Growth still matters, but only when it compounds economically.

The shift is structural, not cyclical. Investors have seen enough marketplace failures to know that early GMV growth without liquidity density is fragile. They are now underwriting across three dimensions:

The best marketplaces don't just facilitate transactions. They become infrastructure layers that coordinate fragmented economic activity, and investors are specifically looking for early signals that a business can reach that level.

2026 has produced a clear market bifurcation: two distinct fundraising environments running in parallel. AI-native marketplaces are raising at elevated valuations on the strength of technical differentiation and growth velocity. Traditional marketplaces (even strong ones) face a more rigorous bar: investors expect demonstrated unit economics, proven retention, and a clear path to platform-level defensibility. If you're building a traditional marketplace, the benchmarks in this guide are your reality. If you're building AI-native, the ceiling is higher, but so is the scrutiny on whether the AI is creating real behavioral change or just a better interface over the same underlying dynamics.

Marketplaces are among the most powerful business models in technology because of network effects. As supply grows, demand improves. As demand grows, supply becomes more valuable. When this flywheel works, acquisition costs decline, retention strengthens, and the business becomes increasingly difficult to displace.

But that same structure makes marketplaces extremely difficult to launch. Every marketplace must solve the cold start problem: attracting supply and demand simultaneously, in the same geography, at the same time, often before either side sees obvious value in participating. Most marketplace startups fail here, not because the idea was wrong, but because they tried to scale before achieving transaction density.

The strongest marketplaces resist the temptation to grow too fast. They start in narrow verticals or geographies, prioritize high-frequency workflows, and build repeat transaction loops before expanding. Hipcamp spent years building dense supply in specific camping regions before expanding nationally. Faire launched with a focused set of independent boutiques and artisan brands, proving the market cleared reliably before pursuing broader distribution. This density-first approach is not just operationally sound. It is what investors consistently reward.

Investors are not looking for fast-growing marketplaces. They are looking for marketplaces that demonstrate compounding liquidity. The distinction matters because it defines everything from fundraising timing to how you present your metrics. Fast growth funded by paid acquisition can mask a broken marketplace. Compounding liquidity (where each new supplier attracts more buyers, and each new buyer makes the platform more valuable to suppliers) is what defensibility actually looks like in early data.

The benchmarks below are directional, not prescriptive. Founder background, category dynamics, competitive positioning, and macro conditions all influence outcomes significantly. The right question isn't whether you hit an exact number at an exact moment. It's whether your trajectory is moving in the right direction relative to your category. That said, the floors have risen in the current environment and investors are less willing to underwrite narrative at the expense of evidence.

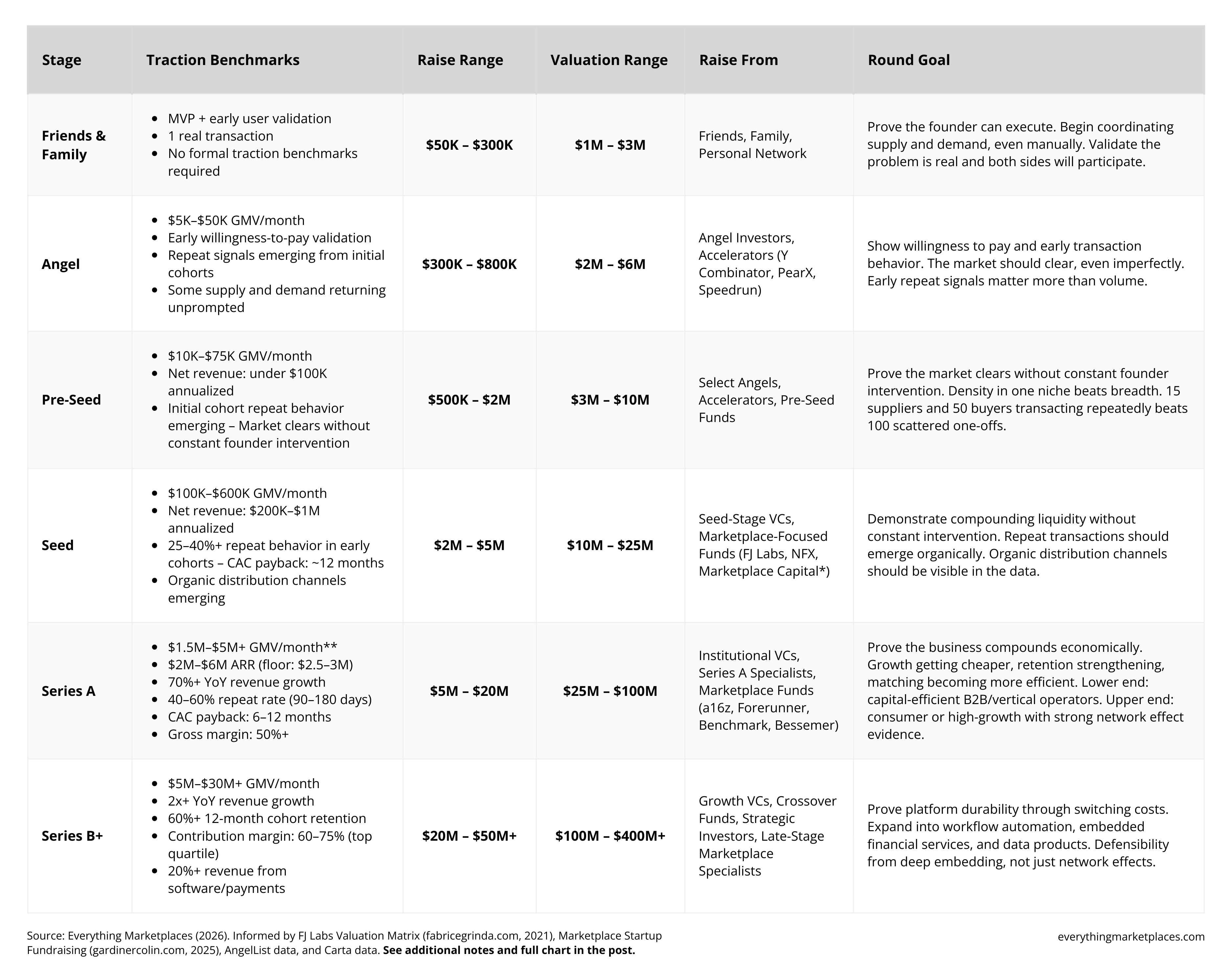

Round Size: $50K–$300K

Valuation: $1M–$3M

Friends and family capital exists to build the first version of the product and test whether real users are willing to participate in the marketplace. At this stage, investors (usually people who know you personally) are betting on founder insight and execution ability, not business metrics.

There are no formal traction benchmarks at this stage. The goal is simply to demonstrate that you can begin coordinating supply and demand, even if transactions are manual. Many of the best marketplace founders start here: doing things that don't scale to understand how their market actually works. Paul Graham famously advised founders to do things that don't scale deliberately. The insights from manual coordination inform product decisions that can't be learned any other way.

Key signals: Early market insight, evidence of founder conviction, initial conversations with supply and demand, and, ideally, at least one transaction that happened because you made it happen.

Round Size: $300K–$800K

Valuation: $2M–$6M

Angel rounds are where real product-market signals begin to matter. Investors want to see willingness-to-pay validation, early transaction behavior, and initial signs of repeat usage. These don't need to be polished. They need to be real.

Many successful marketplaces at this stage still operate manually behind the scenes. This is not a weakness. It often demonstrates that the founder understands how liquidity is actually created in their market, and that they're prioritizing real economic activity over premature automation. The Airbnb founders famously photographed listings themselves in the early days. Whatnot's early team manually managed seller onboarding before building tooling to automate it.

Key traction benchmarks:

Round Size: $500K–$2M

Valuation: $3M–$10M

At pre-seed, investors are underwriting founder insight and early market validation rather than business performance metrics. Strong pre-seed founders understand not just customer problems, but how transactions actually occur inside their industry: the informal workflows, trust patterns, and friction points that determine whether supply and demand will actually transact.

The primary goal is proving that the market actually clears. Supply and demand concentration in a specific niche often matters more than total transaction volume. Showing that 15 suppliers and 50 buyers are transacting repeatedly in one specific geography or vertical is more compelling than 100 one-off transactions spread across different contexts. Density of activity beats breadth of reach at every early stage.

Key traction benchmarks:

Most important: evidence that supply and demand are meeting and transacting without constant founder intervention. That's the first sign the market can clear on its own.

Round Size: $2M–$5M

Valuation: $10M–$25M

Seed stage is where liquidity must begin compounding without constant founder intervention. Investors want to see repeat transactions, pricing validation, and early organic distribution channels. They are evaluating whether the marketplace is on a path to self-sustaining liquidity, or whether it requires continuous manual support to function.

Retention is often the most important predictor of long-term marketplace success at this stage. Strong seed-stage marketplaces typically demonstrate 25–40%+ repeat transaction behavior within early cohorts (though this varies meaningfully by category frequency; a daily-use service marketplace and a once-per-year specialty marketplace are not directly comparable).

Key traction benchmarks:

Strong seed marketplaces also show organic distribution channels emerging: reputation effects, workflow adoption within a professional community, or industry referrals. These are early signals that liquidity is beginning to compound on its own, which is ultimately what every investor at this stage is looking for.

A note on Seed+ and bridge rounds: A meaningful number of marketplace founders who raised pre-seed and seed rounds at 2021-era valuations are now navigating extension rounds before reaching Series A thresholds. This has become a standard part of the fundraising landscape. If you find yourself here, the clearest path forward is demonstrating a specific economic inflection point (not just more of the same growth) that justifies the bridge and resets the conversation with institutional investors.

Round Size: $5M–$20M

Valuation: $25M–$100M

Series A is the first true institutional validation round. Investors at this stage are deciding one thing: will this company become a platform, or stay a transactional product? The signals they're looking for shift from growth velocity to economic compounding and early network effects.

The framing matters: investors aren't just asking whether you're growing, but whether growth is getting cheaper, retention is strengthening, and supply-demand matching is becoming more efficient. Faire's Series A story was built on exactly this: exceptional supplier retention and clear evidence that buyers were discovering and returning to brands they wouldn't have found elsewhere. The matching was demonstrably better than alternatives. That's what a defensible marketplace looks like in early data.

The lower end of the raise range reflects capital-efficient B2B and vertical marketplace operators who hit these benchmarks without requiring large capital outlays; the upper end reflects consumer or high-growth categories with strong network effect evidence and larger TAM stories.

Key traction benchmarks:

Strong Series A marketplaces show declining CAC over time, improving retention curves across cohorts, and early evidence of network effects that make supply or demand acquisition progressively easier. These are the signals that justify the valuation step-up from seed.

A note on the revenue threshold: The Series A bar has moved materially since 2021. The current practical floor is $2M–$3M ARR with strong growth. Investors who previously backed companies at $1M ARR are now consistently waiting for higher conviction signals before committing institutional capital. Founders who plan their Seed runway assuming a $1.5M ARR Series A threshold are likely to run short.

Take rate context for GMV benchmarks: GMV figures throughout this guide require take rate context to be meaningful. A consumer marketplace at a 15% take rate generating $2M/month GMV produces $3.6M ARR, which is a strong Series A story. A B2B marketplace at a 4% take rate generating the same $2M/month GMV produces only $960K ARR, well below the institutional threshold. B2B marketplace founders need approximately 3–4x higher GMV than their consumer counterparts to reach the same net revenue benchmark. Always present GMV alongside your take rate and net revenue when fundraising.

Round Size: $20M–$50M+

Valuation: $100M–$400M+

Series B is where the platform thesis gets tested. The strongest marketplaces at this stage have expanded beyond transaction matching into adjacent value layers: workflow automation, embedded financial services, and data and intelligence products.

This expansion matters because defensibility increasingly comes from switching costs, not just network effects. A marketplace embedded in a supplier's daily workflow (through payments, financing, analytics, or operational tooling) is far harder to displace than one that only facilitates matching. Faire's embedded financing and net-terms product created switching costs that pure matching competitors couldn't replicate. Whatnot's live commerce infrastructure became integral to how sellers built their audiences, not just where they transacted.

Key traction benchmarks:

Stage-by-stage benchmarks for marketplace founders: traction required, who to raise from, and what each round is designed to accomplish.

Note: These ranges reflect current market conditions and are directional, not prescriptive. Founder background, category dynamics, growth trajectory, and competitive positioning can shift outcomes significantly in either direction. The standard deviation around these medians is wide, and exceptional companies frequently exceed the upper bounds.

* Disclosure: Marketplace Capital is the author's pre-seed/seed-stage fund. Its inclusion reflects actual investment focus, not a paid placement.

** Series A GMV is highly take-rate dependent. B2B marketplaces (typically 3–8% take rates) require significantly higher GMV than consumer marketplaces (10–20%) to reach the same net revenue threshold. Always present GMV alongside take rate and net revenue when fundraising.

Typical dilution by stage (directional): Friends & Family 5–20%, Angel 15–20%, Pre-Seed 15–20%, Seed 17–20%, Series A 17–20%, Series B 15–18%. See the Marketplace Fundraising Quick Reference in the post resources for additional context.

Fundraising timelines vary significantly by category and macro environment. The ranges below reflect directional patterns based on typical marketplace progression:

Stronger companies with high liquidity density and improving unit economics tend to compress these timelines. Companies with weaker retention or capital efficiency often experience elongated fundraising cycles, which is why retention quality at early stages matters so much. A marketplace that retains well almost always fundraises better, because the data is inherently compelling.

In the current environment, investors prefer clear economic inflection points between rounds rather than rapid sequential raises. The signal they are looking for: something materially improved since the last raise, not just more of the same. The question to answer before starting each raise is not "have we grown enough?" but "what is fundamentally different about our business now?"

The benchmarks above are starting points. Several structural factors can meaningfully shift where a given company falls in those ranges, compressing timelines, expanding valuation multiples, or in some cases making fundraising significantly more difficult. Understanding these factors before you start raising is as important as knowing the numbers themselves.

Vertical Selection

Category selection is the most consequential decision a marketplace founder makes. More consequential, over time, than go-to-market strategy, team composition, or even product. The unit economics ceiling of a given vertical is largely fixed by the structure of that market: transaction frequency, average order value, take rate tolerance, and supplier switching costs. A founder can execute flawlessly and still face a structural ceiling that makes the business uninvestable at scale.

B2B service marketplaces, workflow marketplaces, and embedded financial marketplaces tend to outperform because they have stronger retention and higher switching costs. Buyers return frequently because the marketplace has become part of their operational workflow, not just a discovery tool. Faire in wholesale retail, Procore in construction, and Workrise in energy services all built retention advantages rooted in workflow integration, not just network effects.

Low-frequency consumer marketplaces and commoditized supply markets face more fundraising volatility. Higher customer churn, weaker pricing power, and thinner margins make the economic compounding story harder to tell at early stages. This doesn't mean these categories can't produce great businesses, but founders in them need to find specific structural advantages (geographic density, exclusive supply, proprietary matching data) that compensate for the inherent churn dynamics.

The best time to pressure-test your vertical selection is before you build. The worst time is when you're sitting across from a Series A investor who tells you the category structurally can't support the take rate and retention economics they require — and they're right.

Marketplace + SaaS Hybrid Models

One of the most important structural shifts in modern marketplace investing is the rise of hybrid models that combine transaction economics with recurring revenue software. Marketplace + SaaS businesses tend to receive premium valuations because recurring revenue improves forecasting reliability and reduces business volatility.

Strong hybrid companies show early MRR signals alongside transaction revenue. Investors prefer businesses that can demonstrate predictable base revenue supporting marketplace expansion. The SaaS floor gives the marketplace ceiling more credibility. A marketplace doing $800K GMV/month with $150K MRR in software subscriptions is a materially different and more fundable business than one doing the same GMV without the recurring layer.

AI-Native and Agentic Marketplaces

AI-native marketplaces represent one of the fastest-evolving categories in 2026. These companies use AI to automate matching, optimize supply allocation, or enable agent-driven execution. AI can accelerate liquidity formation by reducing operational friction and improving supply productivity in ways that were impossible for previous generations of marketplaces.

However, AI alone does not create a defensible marketplace. Investors still require evidence of real behavioral marketplace activity: dense supply-demand interaction, repeat transactions, and durable network effects. The AI layer can improve efficiency and compress the timeline to liquidity, but it cannot substitute for the underlying economic behavior that makes a marketplace valuable. The companies that will win in this category are those where the AI is creating measurably better matches, not just a faster interface over the same underlying market dynamics.

The benchmarks in this guide reflect the traditional marketplace bar. The ceiling for AI-native marketplaces is materially higher when the AI is genuinely changing market behavior. Mercor, an AI-powered hiring platform matching engineering and technical talent at a scale and speed manual recruitment cannot replicate, is a clear example: rapid growth and fundraising at valuations well above traditional marketplace comps, driven by investor conviction in matching that demonstrably outperforms manual alternatives. These outliers exist, but they are underwritten on fundamentally different terms. The AI has to be doing real work, measurably changing how supply and demand find each other, not simply automating what was already happening.

Accelerator Signaling

Top-tier accelerators can meaningfully impact fundraising dynamics. Programs like Y Combinator, PearX, and Speedrun create investor competition during fundraising through curated access, structured demo day processes, and strong alumni signaling effects.

In practical terms, this can translate to slightly higher valuation ranges at pre-seed and seed, faster closes, and more competitive term dynamics. However, accelerator affiliation does not replace traction. Over time, market pull and economic performance dominate signaling effects. The accelerator halo fades; the metrics don't.

Marketplace fundraising in 2026 is defined by capital efficiency, real economic activity, and defensible product advantages. Not growth narratives alone. The question investors are asking at every stage is not "how fast are you growing?" but "why does your marketplace become harder to displace over time?"

The strongest marketplace companies in the current environment are not necessarily the fastest growing. They are the ones that can demonstrate their economics improve as transaction volume increases: declining CAC, strengthening retention cohorts, rising take rates, and expanding contribution margins.

The biggest mistake marketplace founders make in 2026 is optimizing for the fundraising benchmark rather than the underlying behavior that makes the benchmark meaningful. Hitting $2M ARR through one-time transactions and paid acquisition is not the same business as $2M ARR built on repeat behavior and organic growth. Experienced marketplace investors know the difference the moment they see cohort data.

Practical implications for founders:

If you can demonstrate that your marketplace becomes more efficient over time, that the flywheel is real and accelerating, you will be positioned to raise capital more effectively and build a business that can function as long-term economic infrastructure. That is the standard the best marketplace investors hold, and the right standard to hold yourself to.

For additional perspective on marketplace benchmarks and valuations, see the FJ Labs Valuation Matrix published by Fabrice Grinda of FJ Labs.

Note: The FJ Labs Valuation Matrix was originally published in 2021. Marketplace investors reference the benchmarks and in large part confirm they remain directionally representative, though some of the valuations, revenue thresholds, and expectations have moved upward since the original publication. This guide incorporates those updated expectations. The FJ Labs matrix provides useful additional context on valuation multiples and category-level nuance across stages.

Downloadable reference materials to accompany this post:

I'd love to hear what you're seeing in the market. Share your experience in the comments below, whether you're actively fundraising, recently closed your round, or from the investor side. The benchmarks in this guide are only as useful as the real-world context everyone adds to them.

Thanks to Jeff Weinstein (FJ Labs), James Currier (NFX), Jason Bornstein (Forerunner), Matthew Brown (Headline), Sonia Nagar (Snak VC), Colin Gardiner (Yonder Ventures), and Andrew Blachman (Marketplace Capital) for reviewing an earlier draft of this guide.

You can connect with Mike to discuss this post in the Everything Marketplaces community here.